Recently I structured an Equity Development Partnership, our safer alternative to partnerships, for a practice owner and an associate dentist. I assumed that they were happy and doing well until I received a call from the owner that the associate was making too much money and that the owner was losing money. Apparently, while still less than six months into the relationship, the associate was producing $50,000 per month and increasing. The owner anticipated that the associate would produce as much as $70,000 per month before the end of the first year. He and his accountant were seriously concerned about the losses he would incur as a result of paying an associate commission of $250,000 or more, along with the additional overhead for the additional production that the owner would have to pay.

This owner and his accountant's concerns are not unusual when dentists believe that the traditional view that overhead is a fixed percentage that applies to total income. While the overall overhead of many general practices may be in the range of 65%, that figure, while accurate, is also misleading. The principle that provides the most insight into the most successful management of a practice however, is the Incremental Income Principle.

Here's how the Incremental Principle works in dentistry. This principle realizes that most dental practices have a break-even point in the range of $200,000. This means that the overhead on the first $200,000 is 100%. This initial $200,000 of revenues covers the fixed costs, such as, rent, insurance, utilities, telephone, etc., and the associated variable expenses for that production, such as salaries, laboratory, supplies, and so on. (Some people consider salaries to be a fixed expense, but I consider them to be variable, because unlike rent, utilities, insurance, and the like, salaries can be adjusted almost immediately by hiring or laying off employees. They also bear a proportional relationship to gross revenues.)

Additional increments of income of $100,000 only incur the variable expenses required to produce that amount. The fixed expenses have already been paid whether any additional revenues were produced or not. The only extra expenses on these additional revenues are laboratory, supplies, and other miscellaneous expense, which are generally no more than 25% in most practices. Therefore, additional incremental income blocks of $100,000 will yield around 75% net or $75,000 of income each.

This is why it is less risky to spend more money to buy a large practice than spending less money to buy a small practice. Larger practices, while having a greater debt exposure, have a lower risk because there is a greater margin over the break-even point. Small practices, which have less debt exposure, are much riskier because the gross revenues are closer to the break-even point, and a slight drop in revenues can wipe out any and all profitability while a small drop in a large practice will still yield a large net income.

Now, let's apply the Incremental Income Principle to associateships. In considering adding an associate to a practice, I look for what I call the "phantom practice", which is the potential for available Incremental Income. If there is no available excess production for an associate to treat, there is no need for an associate and attempting to add one would only result in a frustrating experience for the owner, the associate, the staff and the patients.

The phantom practice represents the treatment that the owner cannot or will not produce. It may involve any endo, perio, surgery or other treatment modalities that the owner chooses not to do. It can also include the patients that cannot be seen on a timely basis because the owner is already booked too far out. The only way the phantom practice can be realized and the incremental income and profitability made real is by adding an associate dentist to treat those "surplus" patients and perform those services not performed in office.

If there is a phantom practice present and an associate is brought in to service it, the extra expenses for such production are only the variable expenses that accompany incremental income, plus the commission paid to the associate and a salary for an assistant. While the total variable overhead expenses for the phantom practice may approach 75%, this still results in a 25% profit from the associate's production.

Getting back to our dentist owner with the dilemma of losing money on his associate, I scheduled a conference call with the owner and his accountant. We set up an internet meeting so everyone could view and work with a spreadsheet that I had created to find out where the money was being lost. In the case of the subject practice, in addition to the expected extra variable expenses, there were additional fixed expenses that had to be considered. New office space had to be built out at extra cost, and extra rent and utilities would be incurred. An additional highly paid assistant was also hired, and new equipment had to be purchased. Further expense was spent on increased marketing and benefits for the associate.

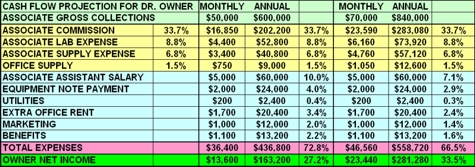

The teleconference with the owner and his accountant was an interactive session, with input from all parties being included in the analysis. By the end of the meeting, all of the data, assumptions, and calculations were agreed to and accepted by the owner, his accountant, and myself. The following spreadsheet displays the income and expenses as a result of the addition of the associate dentist in this particular practice. The incremental variable expenses are highlighted in yellow and the additional fixed expenses are highlighted in blue. Figures were calculated for associate production of both $600,000 and $840,000 per year.

In spite of the extra expenses for additional rent, equipment, salaries, employee benefits, and marketing, as well as the typical additional variable expenses for lab and supplies, at the associate production level of $50,000 per month, the owner would still realize an annualized profit of $163,000 per year, a 27% profit.

The owner's concerns about high expenses resulting in large losses to him when the associate's production reached $70,000 per month were examined as well. His concerns were allayed when it was found that the profit increased to over $280,000, or 33% of revenues. If the owner were not required to rent more space, buy more equipment and spend more on marketing, the profit for both income scenarios would be increased by an additional $72,000 per year.

The key to understanding associateship profitability is to understand the Incremental Income Principle. While the traditional 65% overhead statistic may be true in an overall sense, it ignores the tools for making the best informed decisions regarding income and expenses in your practice, and can result in inaccurate decisions that are very costly or result in your missing a very successful opportunity.

An example of being misled by the traditional 65% overhead statistic is the story of a new graduate who started a practice from scratch some years ago. The first year's revenues were $150,000, which was the break-even point for that practice, so his first year net income was zero. He had been told that a practice should have overhead of 65% and a net of 35%, and he figured that he should have netted $35,000. He concluded that there was something wrong with this practice, so he started a satellite practice in the second year in order to earn an income. The second year he grossed $150,000 in the original practice and $150,000 in the satellite practice. His net income from the two practices was still zero.

Had he understood the Incremental Income Principle, he would have concentrated his efforts on his original practice, realizing that there was nothing wrong with it, and that any increase in that practice would have resulted in an 80% net, instead of a second practice with a second break-even point to make.

Another established dentist was considering terminating his associate who was treating the endo and perio in the practice because the owner wasn't making any money from the associate's work. The owner "knew" that his overhead was 60% and he was paying the associate a 40% commission for the work he did, the owner figured that there was no profit for him. I asked the owner if he would do the endo and perio himself when he fired the associate, and he said no, he would refer that treatment out. Then I asked the owner what other expense he incurred from having the associate, and he said there were none, as the associate paid for his own supplies and assistant, and there was no lab expense. We then came to the conclusion that out of 100% incremental income, the only expense was 40%, leaving a profit to the owner of 60% of the associate's revenues. Once the owner realized he was making a 50% higher percentage net for the work that the associate was doing, than for the work the owner did himself, he decided to keep the associate.

The benefits of knowing and using the Incremental Income Principle are critical in the management of dental practices. Conventional wisdom of knowing overhead is traditionally 65% could have led to abandoning considerable profits from terminating an associate, or having a satellite office with another large break-even gross to meet without netting any income. On the other hand, applying the Incremental Income Principle can help a dentist make the safest and most profitable decisions when it comes to practice management.

Add me to your address book

Add me to your address book